June 2024

We get many questions these days about mortgage rates and if they’ll go down. We have no way of forecasting borrowing costs but thought it would be of “interest” to share some history on the changes in home loan borrowing rates. Long story short, mortgage rates are higher than in recent years but very much in line with historical levels.

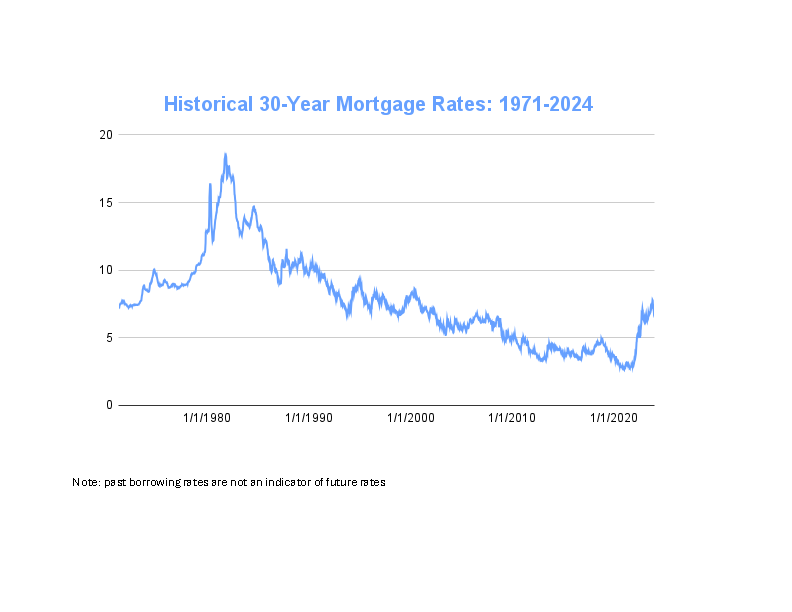

Mortgage Rate History

While home mortgages actually entered the U.S. housing market in the early 1930s, we are going to focus on the past five-plus decades. Between the early 1970s and today, the average borrowing rate on a 30-year mortgage peaked in 1981 at approximately 16%. Consequently, the average 30-year rate got to a low of just under 3% in 2021. Today, as depicted in the attached chart below, the average 30-year mortgage rate is just over 7%, similar to the borrowing costs in the late 1990s as well as the early 1970s.

Decade by Decade Trends

1970’s

The 30-year fixed-rate mortgage, the most common home loan, started off the decade at 7.3% in 1971. By the end of the decade, the 30-year rate was at just under 13%. During the 70’s, the Federal Reserve’s expansionary policy and other factors helped drive up inflation as well as borrowing costs.

1980’s

At the beginning of 1980, homes in the U.S. cost on average $64,000 (source: Department of Housing and Urban Development (HUD)). By 1990, the median price had risen to about $124,000 Brought on by soaring inflation, the 30-year fixed mortgage rate reached 18.4% in October, 1981. Once the Federal Reserve Board (The Fed) was able to tame inflation, the 30-year rate made its way down to 9.78% by the end of the decade.

1990’s

The 1990s brought on quite a change in the 30-year rate, which dropped to an average of 6.91% in 1998. This was partly caused by the dot-com bubble, when many investors exuberantly gobbled up stocks from technology companies that were beyond overvalued. As these stocks decreased in value towards the end of the decade, investors quickly started to focus on fixed-income investments, mostly treasury bonds. The rapid surge in bond buying forced a sharp increase in bond prices and a subsequent fall in bond yields (the “seesaw ePect” is essentially when bond prices go up, bond yields go down, and vice versa). And, as a result, mortgage rates, which follow the 10-year Treasury rate, also declined.

2000’s

Following the dot-com bubble in 2000, and after little change at the start of the new millennium, 30-year mortgage rates fell sharply when the housing market crashed due to the subprime mortgage crisis in 2008. The average 30-year fixed mortgage rate dropped from 8.08%in 2000 down to 5.38% by 2009. The Fed swiftly put into place quantitative easing measures by purchasing large amounts mortgage bonds, which quickly drove down interest rates and subsequently kick-started the economic recovery.

2010’s

Last decade, the 30-year mortgage rate continued to trend downward, beginning in the 4% range and essentially holding close to that mark throughout the ten years, ending slightly lower towards the end. These historically low rates were brought on in part by the Fed’s pull-back on bond-buying.

2020’s

2020 saw new lows for mortgage rates, with the 30-year fixed rate diving to just under 3%, averaging 3.38% for the year. Amid the Pandemic, fearful investors fled to more stable products such as Treasury and mortgage bonds, pushing yields — and borrowing rates — even lower. Rates began to creep back up in 2021, but the ongoing Pandemic ultimately tempered their rise.

Then came 2022 and into 2023. Determined to curb rising inflation, the Federal Reserve began raising its benchmark interest rate. In October 2022, the 30-year rate rose past 7%. By October 2023, the 30-year broke through 8%. As of recently, the rate is approximately 7%.

Lower mortgage rates often spur demand for home buying and can increase buying power. Of course, higher rates result in higher monthly mortgage payments, which can be a barrier for some buyers. Borrowers with higher credit scores, stable income(s) and larger down payments might qualify for lower rates. Hence, while one should keep an eye on mortgage rates, it’s often not wise to time the market. While a home is an investment, it’s also where you live.

In closing, the best time to purchase a home is when the time is right for you. Borrowing rates may simply add to the overall cost of doing so. Thank you for reading our latest thoughts and please call us at any time with your financial planning questions.

Sources: Bankrate and Freddie Mac

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.